Lead image via

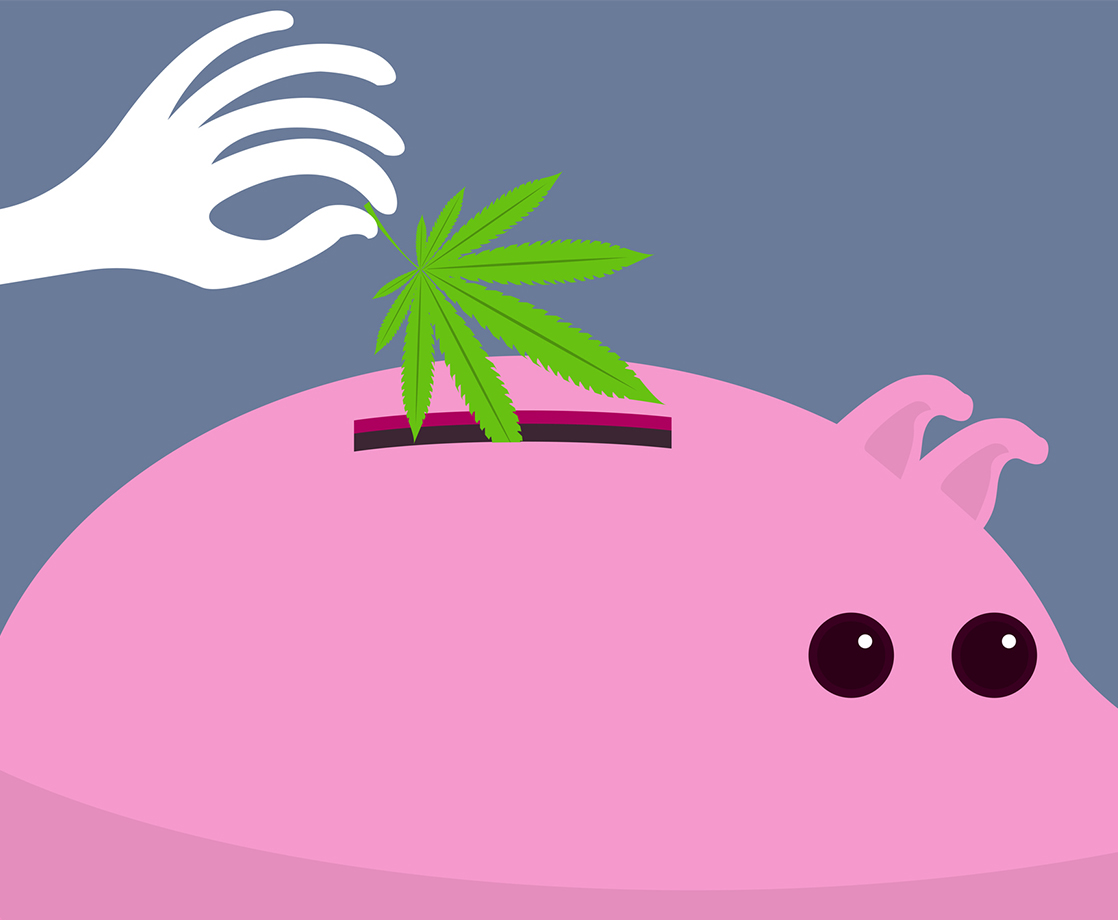

Although federal law prohibits banks from serving any business that handles a federally-prohibited drug, including marijuana, more and more banks are willing to accept multiple types of green. According to new federal data spotted by cannabis activist Tom Angell at Forbes, the number of banks who have made the risky decision to serve canna-businesses increased throughout 2017. The report was published by the Financial Crimes Enforcement Network (FinCEN), and it indicates that the number of financial service providers actively serving canna-businesses increased from 318 in September, 2016 to 400 in September, 2017.

Attorney General Jeff Sessions has constantly threatened to crack down on states that have legalized cannabis, but the Department of Justice continues to operate under Obama-era cannabis policies. The Cole Memo, authored in 2013, limits the federal government's ability to interfere with state-legal cannabis activity. In 2014, the Treasury and Justice Departments issued guidance to banks instructing them how to serve the cannabis industry without violating federal law.

As part of this guidance, banks are required to notify FinCEN of potentially illegal activity via Suspicious Activity Reports (SARs). The agency classifies cannabis-related SARs in three categories. The Marijuana Limited filing means that a bank is dealing with a canna-business that is fully compliant with state laws and is protected by the Cole Memo. The Marijuana Priority filing is for banks dealing with businesses that are under criminal investigation or not protected by the Cole Memo. And the Marijuana Termination filing is for banks that have ended their relationship with canna-businesses. The majority of SARs that FinCEN receives are Marijuana Limited filings.

The lack of access to financial institutions is an omnipresent hurdle throughout the legal cannabis industry. Canna-businesses are forced to make all of their transactions in cash, which they must store and transport themselves. And thanks to section 280E of the federal tax code, canna-businesses cannot claim the same deductions and credits that all other businesses can, effectively raising their tax rate to 80%. Businesses that collapse under this financial pressure cannot even avail themselves of the standard bankruptcy protections available to all other industries.

Although the increase in banks' willingness to serve canna-businesses seems promising, Jeff Sessions has continuously threatened to change the Justice Department's cannabis policies since Trump appointed him to office. Numerous politicians have proposed legislation to block federal authorities from punishing banks willing to serve the industry, or to repeal the 280E tax code, but none of these attempts have succeeded to date.

In the meantime, cannabis entrepreneurs have been brainstorming alternative ways to solve the industry's financial obstacles. A new app called CanPay has launched in several canna-legal states, and it allows customers to purchase cannabis using a phone app. CanPay transfers the payment from the buyer's checking account to the Colorado Credit Union, one of the few banking institutions that currently accepts cannabis industry clients. Others in the weed game are looking to blockchain-based payments as a solution, including (supposedly) the rapper The Game. Blockchain, the encrypted technology behind Bitcoin, could be used to track legal cannabis products from seed-to-sale, as well as provide a legal, discrete payment system for purchases.